Weekly Legislative Update

May 26, 2020

SBA Releases PPP Loan Forgiveness Application

On May 15th, the Small Business Administration (SBA) released that application that businesses will submit to their lender to apply to have their Paycheck Protection Program (PPP) loans forgiven. The application, which is accompanied by a number of worksheets and instructional pages, provides clarity on a number of critical questions that were facing PPP loan recipients.

There are still some open questions and we anticipate that, in addition to the application document, the SBA will be releasing interim rules relating to the loan forgiveness provisions. In the meantime, businesses that received a PPP loan, are well advised to review the application and accompanying guidance as soon as possible, rather than waiting until the end of their loan period, in order to identify and take any necessary steps to ensure and maximize loan forgiveness.

The biggest new takeaways from the application are as follows:

The Covered Loan Period

Pursuant to the CARES Act, which established the PPP loan program, the relevant period for the purposes of calculating loan forgiveness is the 8 week (56 day) period after the loan proceeds are received by the company - referred to as the "Cover Period." To simplify the loan forgiveness calculations, the application provides businesses that pay employees on a biweekly or more frequent basis the option to elect an "Alternative Payroll Covered Period" to better track with their pay periods. Specifically, instead of calculating the eight week period as beginning on the date the loan proceeds are received, such businesses can instead elect to calculate the eight week period starting on the first day of the first payroll following that date (this alternative eight weeks is referred to as the "Alternative Payroll Covered Period"). This will allow businesses to line up the eight week period with their normal payroll schedule rather than having the eight week period cover multiple partial pay periods.

Businesses that may be interested in utilizing the Alternative Covered Payroll Period for the purposes of their loan forgiveness calculations and application should be aware of two important things:

- This option is only available to businesses that pay employees in a biweekly or more frequent basis. Therefore, businesses that pay employees twice per month (or less frequently than biweekly) are not eligible to use the Alternative Cover Payroll Period.

- If a business elects to use the Alternative Payroll Covered Period, this is the eight week period that will apply for the purposes of assessing and calculating loan forgiveness - including with respect to non-payroll expenses. Thus, businesses should assess the impact that electing the standard Covered Period versus the Alternative Payroll Covered Period, or vice versa, will have on the ability to include other eligible costs in the forgiveness calculation.

Calculation of Forgivable Expenses

One of the big open questions left by the CARES Act was what would happen to payment obligations that were incurred but not paid within the eight week loan period or, on the flip side, payments that were made on obligations that weren't incurred during the eight week loan period. The new application provides clarity on these questions as to both payroll and non-payroll expenditures.

Payroll Costs

Per the CARES Act, payroll costs are included in, and are, in fact, intended to be a central part of, the forgivable loan amount. Payroll costs include compensation to employees of up to $15,385 per employee during the 8 week loan period (which would annualize to $100k), plus employer contributions towards group health insurance, retirement plans or employerstate and local taxes on employee compensation. For loan forgiveness related to payments to business owners, the application specifies that businesses may only include payments to owner up to $15,385 OR the eight-week equivalent of the owner's average compensation in 2019, whichever is lower. It is unclear whether amounts paid for a business owner's health insurance or retirement plan contributions are included in, or can counted in addition to, those limits.

The application provides that, in calculating payroll costs, in addition to counting payroll costs actually paid during the eight week loan period, businesses may also include payroll costs incurred during the loan period but not paid during the loan period, as long as the costs are paid on or before the next regular payroll date after the end of the loan period. Thus, for example, if the last day of a company's eight week loan period is June 10, but the company's pay period runs from June 1 through June 15, with payday on the 16th, the company would be able to count amounts earned by employees from June 1 through June 10, even though the employees would not actually be paid until June 16 (six days after the end of the loan period). Of course, amounts earned and paid to employees can only be counted once, so the focus would be on amounts paid during the loan period, with amounts earned only being included if they will not be paid until after the end of the loan period. Among the unanswered questions generated by the application's provisions are how certain types of employer retirement plan contributions, beyond the standard matching contribution, would be treated for the purpose of being included or excluded from the forgivable amount. We anticipate additional guidance in the retirement plan area.

Non-Payroll Costs

Similar to payroll costs, the loan application provides businesses with the opportunity to include covered mortgage, rent and utility payments that are either (1) paid during the eight week period or (2) incurred during the eight week period and paid on the next regular billing date (if such billing date falls outside the eight week loan period). Again, these costs can only be counted once. Regardless of the amount of other costs incurred or paid during the eight week period, covered non-payroll costs may only comprise 25% of the total forgiveness amount.

Reductions to Forgiveness

The CARES Act provided that borrowers are eligible to have up to the principal amount of the PPP loan forgiven BUT that the eligible loan forgiveness amount would be reduced if the borrower made certain reductions the employees' salaries or hourly rates or its total number of full time employees. The application materials provides additional insight and information on how these reductions will be assessed and calculated.

Reduction in Number of Full Time and Full Time Equivalent Employees

Under the terms of the CARES Act, a business' eligible forgiveness amount will be reduced if the average number of full-time equivalent employees employed by the business during the eight week loan period was less than either the average number of full time employees employed by the business either (1) between January 1 and February 29, 2020 or (2) between February 15 and June 30, 2019. The business gets to pick which of the two comparison periods it will use and special rules apply to businesses with seasonal workforces. What the CARES Act didn't do is explain how businesses will calculate how many full-time equivalent employees they have. The application materials shed light on this question.

For the purpose of determining loan forgiveness, a full time employee is an employee who typically works at least 40 hours per week. As to employees who work less than 40 hours per week, the employer may choose to either count all of these employees as .5 full-time employees OR do a full time equivalency calculation for each employee by dividing their regular weekly hours of work by 40. For example, for an employee who typically works 30 hours per week, the business could either elect to count him as a .75 full-time employee (30/40) or, to avoid doing individually specific calculations and count him, and any other employee working less than 40 hours per week, as a .5 full-time employee. The business will need to use the same calculation method for calculating full time equivalencies for the eight week loan period and the comparison period. Businesses that have the capacity to do so, may want to run the calculations using both approaches and both comparison periods to determine which is more favorable for them.

To the extent that the average number of full time and full-time equivalent employees during the 8 week loan period is lower than the selected comparison period, the loan forgiveness amount will be proportionately reduced (for example, if the business has 15 full time and full time equivalent employees during the loan period but had 20 full time and full time employees during the comparison period, i.e. had a 25% reduction in headcount, the loan forgiveness will be reduced by 25%).

However, there are two instances where an employer in this situation may not be subject to a reduction in forgiveness, or the reduction may be reduced:

- First, as set forth in the CARES Act and explained in more detail on the forgiveness application, there is a safe harbor for businesses that restore their prior level of full time and full time equivalent employees by June 30, 2020. For a business to qualify for the safe harbor (1) the reduction in employees must have occurred between February 15 and April 26, 2020 and (2) the business must be back to having the same number of full time and full time equivalent employees as it did during the pay period that included February 15, 2020, by June 30, 2020. For the purposes of considering the employee headcount, the focus is simply on the number of employees that the business has at the relevant periods of time. So a business that reduced its workforce between February 15 and April 26, need only bring on the same number of employees that it previously had and need not rehire the exact same individual employees.

- Additionally, the loan application makes it clear that businesses can exclude, and will not be penalized for employees that leave and are not replaced where: (1) the employer made a written offer to rehire the employee during the loan period that was rejected by the employee, (2) an employee is terminated for cause during the loan period, (3) an employee voluntarily resigns during the loan period, or (4) an employee voluntarily requested, and received, a reduction in his/her regular scheduled hours during the loan period.

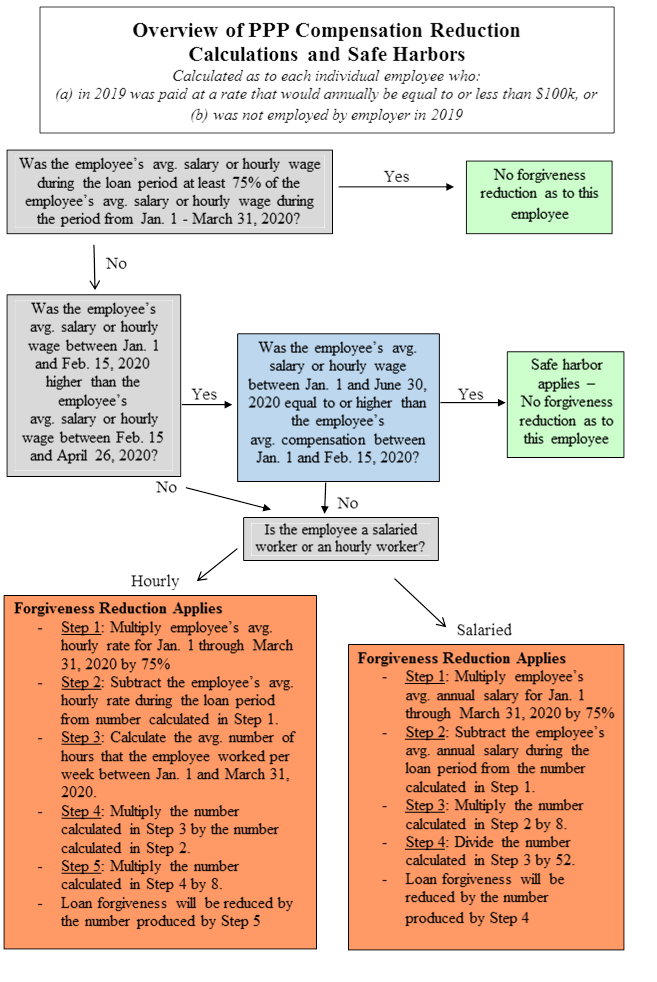

Reduction in Employee Compensation - [Please also see below for a diagram summarizing the following]

In addition to any reduction resulting from a reduction in the number of full time and full time equivalents, the loan forgiveness amount will also be reduced if the business reduces the salaries or hourly rates of employees making equal to or less than $100k annually by more than 25%. This analysis is conducted as to each employee making $100k or less. The process for making these calculations is explained for the first time in the application materials.

First the employee's average salary during the eight week loan period is compared against the employee's average salary from January 1, 2020 through March 31, 2020. This is an important clarification, as the CARES Act was not entirely clear about how businesses would be expected to compare the eight week period against the longer full-quarter period referenced in the law. As was largely anticipated, the application clarifies that the focus will be on the average compensation. If the employee's average salary or average hourly rate during the eight week loan period was at least 75% of the average during the first quarter of the year - the inquiry stops there.

If the employee's average salary or hourly rate during the eight week loan period was less than 75% the average during the first quarter - the business may still qualify for a safe harbor and avoid any reduction in forgiveness. To determine whether the safe harbor applies, the business must first compare the employee's average salary or hourly rate for the year as of February 15 against the employee's average salary or hourly rate from February 15 through April 26, 2020. If the average salary or hourly rate between February 15 and April 26 was less than the average as of February 15 (i.e., a reduction occurred during the Feb. 15-April 26 period), the business can move on to the next step in the safe harbor test. If, the reduction in compensation did not occur between February 15 and April 16 (i.e., the average from that period was the same or greater than the average as of February 15), the safe harbor will not apply and there will be a reduction in the loan forgiveness amount.

For the business that satisfies the first step of the safe harbor analysis, the next step will be to calculate the employee's average salary or hourly rate for the year as of June 30, 2020. If, as of June 30, 2020, the average is at least equal to what it was as of February 15, the employer will be considered to have "restored" the employee's rate of pay and will not be subject to any reduction in forgiveness related to this employee. If the average as of June 30, 2020 is less than the average as of February 15, the safe harbor will not apply and there will be a reduction in the loan forgiveness amount.

For businesses that did not qualify for the safe harbor, as to employees that experienced a reduction in compensation rates greater than 25%, the resulting reduction in the eligible loan forgiveness amount will be calculated depending on whether the employee is paid on an hourly or salaried basis as follows:

Salaried employees - First, the business will calculate the difference between 75% of the employee's average annual salary for Jan. 1 through March 31, 2020 (i.e., what the employee would need to receive not to trigger a reduction) and the employee's actual average annual salary during the loan period. For example, if an employee's average annual salary during Q1 was $100k and the average annual salary during the loan period was $50k, the difference would be $25k (($100k x 75%) - $50k). The difference is first multiplied by 8 and the product is then divided by 52 to calculate the reduction in the amount to be forgiven. Continuing with the example, the reduction in the eligible forgiveness amount related to this hypothetical employee would be $3,846.15 (($25k x 8) ÷ 52).

Hourly employees - First, the business will calculate the difference between 75% of the employee's average hourly rate for Jan. 1 through March 31, 2020 and the employee's actual average hourly rate during the loan period. For example, if an employee's average hourly rate during Q1 was $40 and the average hourly during the loan period was $20, the difference would be $10 (($40 x 75%) - $20). The business would then multiply this difference by the average number of hours that the employee worked per week between Jan. 1 and March 30, 2020 and multiply that number to arrive at final reduction in forgiveness. If the hypothetical employee worked an average of 40 hours per week, the reduction would be $3,200 ($10 x 40 hours x 8 weeks).

In sum, while there may still be more for the SBA, and in turn, PPP loan recipients to determine before the loan forgiveness applications are submitted, the application and accompanying documents go a long way to providing clarity on some of the most pressing outstanding questions.

TIA will continue to advocate for further clarity on the loan forgiveness provisions and support legislative measures to increase the period or flexibility of the PPP loans.